Which Emerging Ecosystem Flywheels are Spinning the Fastest?

Austin, Chicago, Toronto + Waterloo, Atlanta + Alpharetta, and Denver + Boulder lead the list of emerging startup ecosystem activity

In case you haven’t heard yet – Chicago, a city that cherishes its holidays, has instituted a new one: “Unicorn Day.”

This past month, World Business Chicago declared Thursday, June 24th, as “Unicorn Day” in reaction to the number of unicorns (companies valued at over $1 billion) minted in the city. At the time, seven Chicago companies had achieved unicorn status since the beginning of 2021. Incredibly, three additional companies have achieved unicorn status since this announcement.

While the new holiday may be a bit self-aggrandizing for a city of humble midwesterners (and perhaps frothy market dynamics are at play), it’s certainly worth pausing to appreciate just how far our “emerging ecosystem” has come. A decade ago, ten unicorns announced in Chicago over seven months was hard for most to imagine. Today, it is a reality.

For tech hubs, counting unicorns is one of the most popular ways of proving a particular region's startup success and viability. Unicorns breed bragging rights, press coverage, and more investor interest. Unicorns also beget more unicorns as they reach exits, providing employees with the capital to become angel investors or founders themselves.

Chicago’s startup ecosystem appears to be trending in a positive direction. And Chicago isn’t alone. Many emerging ecosystems across the US and Canada are seeing more activity than ever as entrepreneurship becomes more distributed across geographies.

As this trend plays out, I wanted to explore which startup ecosystems located outside of the incumbent tech hubs (California, the US Pacific Northwest, and the US Northeast) have startup ecosystem flywheels that are spinning the fastest.

What is Meant by the Term 'Startup Ecosystem Flywheel'?

This phrase refers to cities or regions with ingredients conducive to generating successful startups in the future. This includes:

Prior successful startup outcomes

Access to talent

Access to angel investors

Access to institutional capital

Quality educational institutions

Nearby Fortune 1000 companies

Supportive startup communities

A population with an entrepreneurial mindset

And other factors that support entrepreneurial activity

In short – an infrastructure that produces and supports quality startups.

For additional context, I like to refer to the Texas Startup Manifesto written by Joshua Baer of the Capital Factory, which discusses many of the critical factors that impact the startup ecosystem flywheel in Texas.

Which Startup Ecosystem Flywheel Indicators Carry the Most Weight?

There are many signs that a startup ecosystem flywheel is spinning within a particular region. However, some indicators are more telling than others. At the beginning of 2021, Bill Gurley tweeted about an indicator that is possibly the most important factor to consider: independent public companies founded in a particular startup ecosystem with a market cap north of $10B.

Gurley's tweet gets at a broader indicator of spinning flywheels in emerging ecosystems. That said, while $10B+ outcomes are certainly the most visible signal, smaller outcomes move the needle as well.

In reality, any company that produces a successful exit/outcome is an indicator of ecosystem success. This is particularly true in the emerging ecosystems – the geographies in which our team at Chicago Ventures is most active. Smaller $100M+ outcomes contribute to $500M+ outcomes, which contribute to unicorn status $1B+ outcomes, which lead to Gurley's $10B+ decacorns.

This begs the question – which emerging startup ecosystems are consistently producing successful outcomes?

The Analysis – Measuring Growth Capital Raised as an Indicator of Ecosystem Success

Let’s put some data behind which startup ecosystems outside of California, the US Pacific Northwest, and the US Northeast have emerging startup ecosystem flywheels that are spinning the fastest.

Ideally, we’d have access to exit value data and would be able to see which markets have the highest number of exits and the largest total exit value. Unfortunately, exit data is generally spotty (i.e. undisclosed acquisition prices).

Instead, we’ll use a good proxy for successful exits – companies that have raised growth capital (defined as $25M+ in total funding). While growth capital is by no means a perfect analog for exits, it's a good indicator that startups are consistently scaling within an ecosystem. We also have quality (but not perfect) data on the funding rounds that are publicly announced.

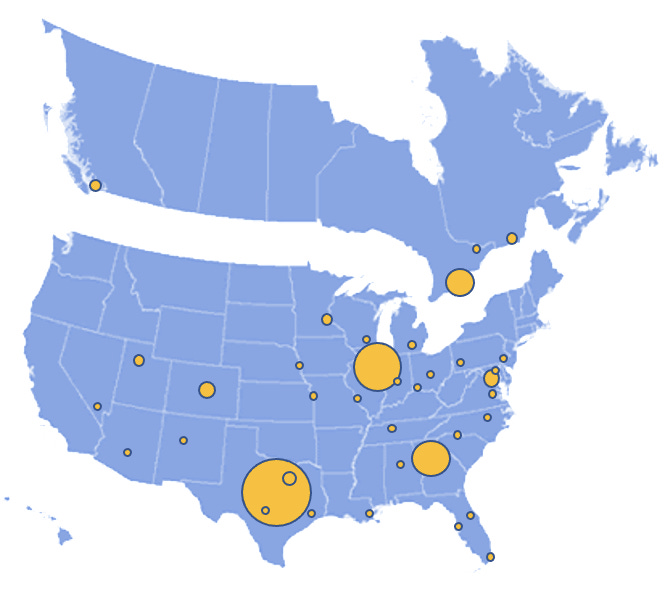

Results: Growth Capital Raised by Ecosystem

Visualization of the most active emerging startup ecosystems ranked by # of companies with $25M+ in funding since 2000

Emerging startup ecosystems ranked by # of companies with $25M+ in funding since 2000 (click on chart to zoom in)

More details on the dataset are in the methodology section below.

Interesting Observations:

The leaders: Austin, Chicago, Toronto + Waterloo, Atlanta + Alpharetta, and Denver + Boulder round out the top five emerging startup ecosystems by this measure.

The power law of startup ecosystems: One of the first things that jump off the page is the power law effect across all ecosystems. The top five ecosystems (out of 39 total) account for over 50% of all companies with over $25M in funding. The top two (Austin and Chicago) account for ~29%. The density of outcomes certainly matters. Successful outcomes lead to more successful outcomes, and the startup flywheel spins faster.

Ecosystem proximity matters: Further, ecosystems within close proximity of each other fuel flywheel momentum. The best example is Texas. Borrowing from the Texas Startup Manifesto 2.0:

“Entrepreneurs should treat the entire state of Texas like one big city — because you can. No matter which city you sleep in, find investors across the state, find customers across the state, and recruit talent across the state. There is nowhere else you can have access to this much market within driving distance.” — Joshua Baer, Founder of Capital Factory

As Joshua notes, the proximity of investors, customers, talent, etc. within Austin, Dallas, Houston, and San Antonio has propelled these Texas cities to become prominent hubs for startup activity.

Don’t ignore the long-tail of ecosystems: While it’s easy to point to the top emerging ecosystems like Austin, Chicago, and Toronto + Waterloo, we shouldn't completely ignore the long-tail of cities. It’s true that only 10 ecosystems had over 20 companies that raised $25M+. The remaining ecosystems were in the range of 0-20 companies. However, the long tail of ecosystems can still produce sneaky outlier outcomes, and some ecosystems have stronger tailwinds than others.

An interesting example is Detroit. Dan Gilbert has tirelessly built up the city for years after his success with Quicken Loans. As a Detroit native, he cares deeply about the city and started many initiatives to develop the city's infrastructure. This includes investment firms (i.e. Detroit Venture Partners), startups, and readily available support for entrepreneurs. A company like StockX is a product of these efforts. When you combine this with proximity to Ann Arbor, don’t be surprised when more outlier outcomes pop up in the region.

Canada thriving 👀 : Three Canadian ecosystems made it in the top 10 (Toronto + Waterloo, Vancouver, and Montreal). Canadian cities grouped together nearly match Texas in terms of growth capital raised. Even I underestimated the startup activity in Canada, and I’m super bullish on the region. Despite the comments of prominent naysayers, the broader Canadian startup ecosystem flywheel appears to be thriving compared to other emerging regions.

Why It's Important

Among the many things I've learned about startup ecosystems and consistently finding quality companies, one factor stands out above the rest – successful startup outcomes beget more successful startup outcomes.

For decades, venture capital dollars have been highly concentrated in three ecosystems: Silicon Valley and the greater Bay Area, New York City, and Boston. According to PitchBook, over 67% of the capital and 41% of the deal count remain within these three regions.

Today, however, these dynamics are changing as entrepreneurship and high investor returns become more distributed across the country. As a result, it feels like a well-established trend that more prominent startups are taking root outside traditional tech hubs. The adage used to be, "You have to be in the Bay Area to get in the startup game." This is no longer the case, particularly as Covid-19 has pushed more startups to operate a distributed workforce and hire remotely.

As this dynamic changes and entrepreneurs start more companies outside of traditional tech hubs, this should change our expectations of where we will find successful outcomes in the future.

From a founder perspective, this changes where I can expect to find concentration of talent, angel investors, institutional investors, customers, and a robust peer group of fellow founders. Perhaps the Chicago founder who was hesitant to take an entrepreneurial leap because of the stigma associated with starting a company in the Midwest can now look at G2, Cameo, Avant, project44, ActiveCampaign, Clearcover, Tempus, Nature’s Fynd, and others as evidence of Chicago’s ability to foster successful outcomes.

Past Performance and Future Success

Past ecosystem performance doesn’t necessarily predict future ecosystem performance. Some ecosystem flywheels have tailwinds making them more prone to producing interesting startups in the future, while other ecosystem flywheels are decelerating.

Miami is a good example of an accelerating ecosystem. Over the course of the past year, Covid-19 has spurred a dynamic where founders, VCs, and other individuals are moving to Miami at an increasing rate. For the past six months, it’s been impossible to log into Twitter without seeing some mention of the Miami tech ecosystem. While the city may have a lower rank today, the influx of ecosystem participants has accelerated the flywheel. I wouldn't be surprised to see Miami jump in the rankings in the coming years.

Another good example is Chicago (though I’m biased on this front). As Chicago continues to mint new unicorns (and new holidays), this will have a tangible impact on the new founders, talent, investors, and entrepreneurial support fostered within the city.

The term “emerging ecosystem” is becoming more of a misnomer by the day…

Thanks to everyone who provided feedback on the post, particularly Abhinaya at M25!

Methodology

The Dataset

I assembled a dataset comprised of tech-enabled companies founded after 2000 in 39 emerging ecosystems in the US and Canada (Note: this data was refreshed as of April 2021). I segmented these companies into the following categories:

Companies that have raised $25-49.9M in total capital

Companies that have raised $50-99.9M in total capital

Companies that have raised $100-499.9M total capital

Companies that have raised $500M+ in total capital

Companies that have IPO'd (Overlap with the prior categories)

Search Criteria

Source: Crunchbase

Data refreshed as of April 2021

All companies founded after 2000

Headquartered in cities listed above

Raised VC funding

Industries Removed: Biotechnology, Genetics, Life Sciences, Therapeutics, Clinical Trials, Medical Device, Health Diagnostics, Biopharma, Health Diagnostics, Renewable Energy, Energy, Restaurants, Food and Beverage, Wine and Spirits, Consumer Goods, Retail, Consulting, Service Industry, Holdings, Industrial, Semiconductor, Mining, Natural Resources, Hardware, Media

Keep in Mind

CrunchBase data isn't perfect

I'm sure some companies will be left out that should not be (hopefully few) – mistakes will be made when sifting through 800+ final companies (and 5000+ to start)

Geography data isn't perfect – i.e. a company located in a far Chicago suburb may not be captured in the Chicago data

However, this data set is certainly directionally correct